This section presents selected work in quantitative research and trading systems. It covers data onboarding, model research and design, deployment, and execution.

My focus is on the full lifecycle of systematic trading, finding an adequate balance between quantitative research and operational trade-offs.

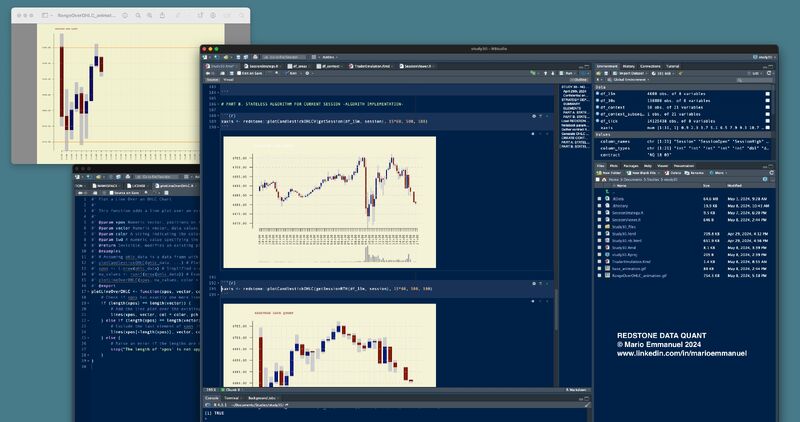

REDSTONE™

Intraday Tick Data Platform

Photo: R-Studio integration of the REDSTONE™ platform — the research environment behind the data framework.

Background

I led the design and operation of the data platform for a small US-registered hedge fund. It was a long project that lasted three years and covered the entire life cycle: prototyping, design, coding, testing and daily operation in production.

The platform processed the entire universe of US equities and options at a large scale, including fifteen years of historical tick data and real-time market snapshots of both options and equities, roughly two billion messages and 1.4 million derivative contracts per day.

Over that period I went through multiple iterations, for some systems as many as seven, steadily refining the platform from the very first limited pipelines into a stable and mature environment. It enabled quantitative research, production models, and the launch of a NYSE-listed ETF by the fund.

Once the project finished I found myself without platform or data but still wanting to pursue my own research on strategies. I wanted to use tick data in the most simple way and on a platform built from scratch. I had very limited resources (both material and operational) so I evaluated different approaches that could be maintained without large budgets but that at the same time would provide all the features you need to do research and operate models in production. I asked myself the following question: how would I face this again from scratch, with more experience and without any of the external constraints present in a corporate environment, what would I do? The answer became something new, simpler, different, and far better once free from those limitations. That is how REDSTONE™ was born.

What is REDSTONE

REDSTONE™ is a data platform crafted from the ground up to serve transparently the data layer for both research and deployed models. It is simple, robust, massively cost-effective, and easy to use for small and medium hedge funds developing and operating futures and OTC strategies. It integrates seamlessly with R, Jupyter Notebooks, and C++ models. While the model currently operates for futures and OTC it can be easily extended to equities or options.

REDSTONE™ is not just a software platform: it includes the industry-specific knowledge and provides the operational answer on how data should be handled in a buy-side operation. It provides small and medium-sized hedge funds and proprietary trading firms with a platform that lets quants focus purely on research while offering a stable, scalable backbone for deployed models, all at a fraction of typical infrastructure costs.

About the name

REDSTONE™ is a fictional mineral in the game Minecraft that is used to build things that do things. It is sort of the energy of the devices built in the game. My son made me play Minecraft for hours and taught me how to use this game mineral to build devices. And since REDSTONE™ is the piece that lets you build and operate models I found it a nice name.

License

REDSTONE™ is licensable to buy-side firms seeking to avoid unnecessary complexity, friction, costs, and delay. While currently designed for OTC and futures, it can be extended to equities and options.

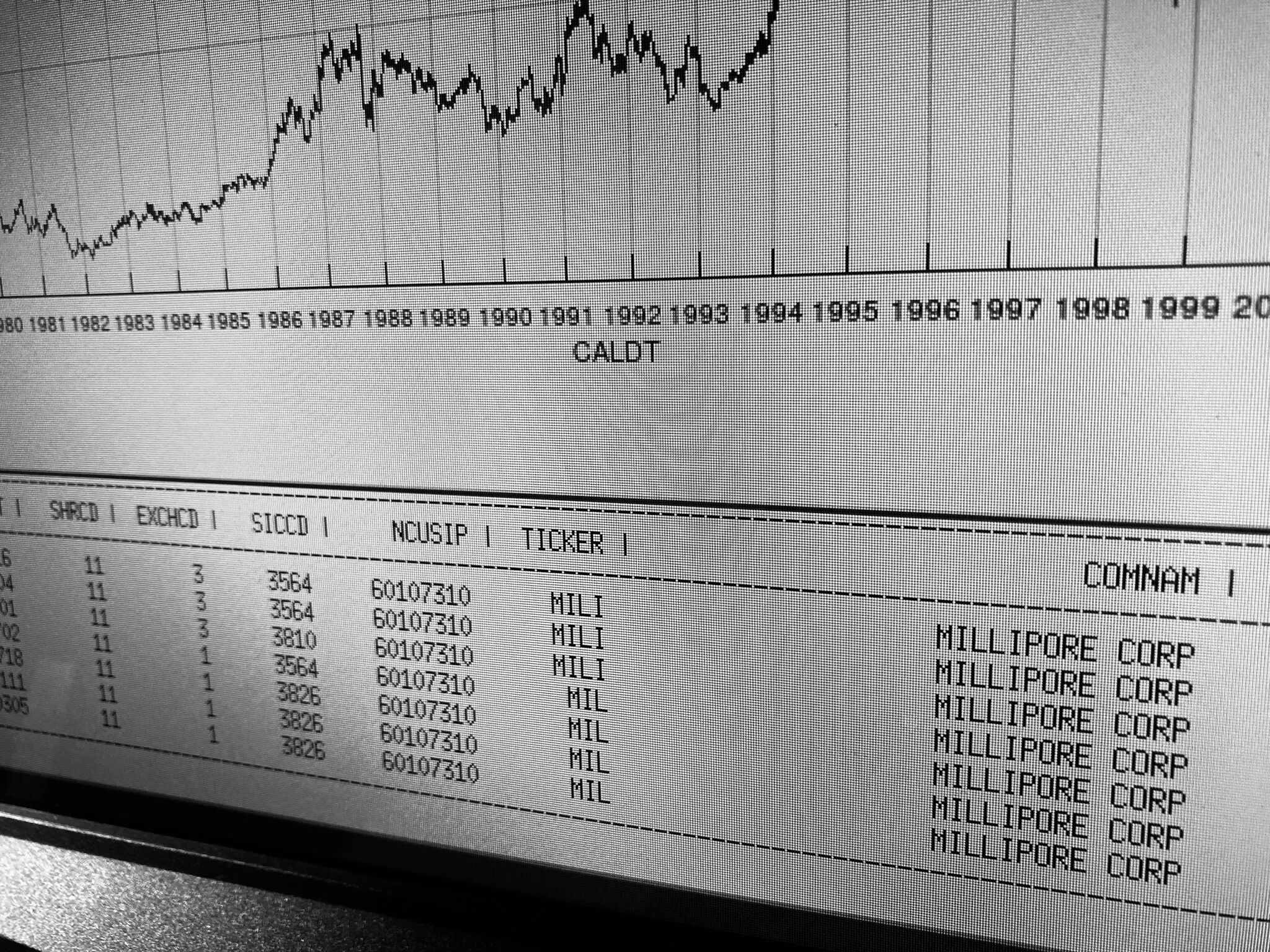

Photo: Long-term price visualization from the ALTONA™ framework.

Background

Intraday and short-term trading are often seen as the most rewarding timeframes, drawing attention to tick data and fast-moving strategies. REDSTONE™ was built for that world; short-term, data-intensive, and immediate reactions.

But what may hold true for a significant part of the buy-side industry is not necessarily true for smaller or larger capitals. The first often lacks the budget to sustain short-term operations; the latter encounters liquidity constraints almost immediately. In many cases, slowing down makes far more sense. Strategies that look beyond the next hour’s volatility spike or the next day’s close are easier to deploy and sustain. They also raise deeper questions about market efficiency and the durability of returns. These questions are often challenged by meta-studies on the sustainability of short-term strategies, and it’s natural, over time, to gravitate from short-term reactions to long-term understanding.

My own interest in how assets relate over months and years eventually matched — if not surpassed — my fascination with intraday dynamics. That shift becomes even more meaningful when you deploy your own capital: your resources are very limited, your perspective widens, and your horizon extends toward your son’s generation, not your next trade. Professionally, too, long-term strategies are where liquidity constraints fade and capital can move more intelligently.

What is Altona

ALTONA™ is a research platform to analyze cross-sectional portfolios and mid- to long-term strategies. It is MATLAB®-compatible and integrates seamlessly with WRDS/CRSP from Wharton, likely the finest financial dataset in existence. The framework simplifies exploration and research, making it possible to study how the structure and behavior of markets change across decades.

With ALTONA™, I moved from intraday trading to developing long-horizon models such as CHROME DOME™. The goal is to study regime shifts and long-term relationships between assets with the same discipline once applied to short-term data. The framework makes handling large datasets simple, so the focus stays on the analysis itself.

ALTONA™ is a technical implementation, but it also reflects a point of maturity and an attempt to look beyond short-term movement and to understand the market’s longer cycles, its underlying patterns, and ultimately, its true story.

About the name

ALTONA™ is named after a district in Hamburg — once Danish, later Prussian, and now simply a district of a German city. It reflects how markets themselves evolve through long histories and transformations.

License

ALTONA™ was built for personal use but can be licensed to hedge funds, proprietary trading or family offices.

CHROME DOME™

Systematic Investment Market Model

Model Scope

CHROME DOME™ is a systematic investment strategy designed as the primary vehicle for managing a private retirement portfolio. It seeks to preserve capital, withstand adverse market conditions, and deliver steady mid- and long-term growth — while remaining optimal under Swiss tax regulations.

Built for resilience, including severe market crashes (scaled mitigation up to 90% drawdown)

Risk adjustment based on entry conditions

Optimized for Swiss tax treatment

Low-cost, tax-efficient instruments

Solid mid- and long-term yield expectations

Diversified across asset classes and structural exposures

Quantitative methodology grounded in empirical evidence

Approach

The model is based on long-term market patterns and macroeconomic cycles. Its rules reflect both historical relationships and forward-looking risk controls. The backtest spans multiple decades and includes varied market environments, interest-rate regimes, and crisis periods.

Particular attention is given to capital allocation under the current market conditions.

Availability and Performance

The model has been deployed with family capital since January 2024. Since inception, it has achieved yield and risk outcomes consistent with its design objectives.

CHROME DOME™ is part of my professional intellectual property. Originally developed for personal use, it may be licensed under appropriate agreements to hedge funds and family offices.

About the Name

Flight paths of the Chrome Dome operation.

CHROME DOME was the codename for the Cold War–era NATO airborne operation designed to ensure survivability and continuous readiness under any circumstance.

Similarly, this investment model is structured for continuity and resilience — built to endure deep market shocks, adapt to changing regimes, and remain operational through every condition the markets may impose.

ABLE ARCHER'25

Eurozone Bonds Rotation Model

Model Scope

ABLE ARCHER'25 is a macro-driven investment model focused on European bonds as part of a long-horizon retirement portfolio.

It seeks to balance stability and yield, while acknowledging the economic distortions and risks caused by recent EU foreign policy decisions.

Design Principles

Allocation limited to EUR and CHF bonds.

Annual rotation and recalibration based on scenario analysis

Multi-model input: interest rate cycles, inflation dynamics, and geopolitical risk

Designed for long-term private capital preservation and income continuity on retirement

Scenario Framework

Each year, the model re-evaluates allocation weights and maturity exposure using a structured set of macroeconomic and geopolitical scenarios.

Opening scenarios include:

Energy and industrial recovery (détente following the collapse of the current political regime in the Eurozone)

Continued Energy and industrial disruption from prolonged proxy confrontation with Russia

Full-scale European economic depression or sovereign default contagion

(Extreme case) direct military escalation or limited TNW exchange scenario in Central Europe

The system treats these as stress boundaries — not forecasts — ensuring that portfolio structure remains coherent even under extreme assumptions.

Methodology

ABLE ARCHER'25 uses a set of macro indicators with corporate credit metrics to guide yearly rebalancing, providing a simple but yet effective way to provide stability and yield.

The rotation mechanism rebalances capital and maturities aligned with the dominant macro regime and the rest of strategies that cover the portfolio.

Model Architecture

Availability and Deployment

The model is designed to be used as part of a long-term portfolio and has been deployed with own family capital in 2025.

Although not designed as a product, it can be licensed to hedge funds and family offices under appropriate agreements.

About the Name

Photo: NATO Able Archer'83 — preparations for a war in Central Europe that could not be fought and a victory that could not exist.

Much like the original Able Archer exercises — the annual NATO maneuvers in Central Europe during the 1980s — the model contemplates a worsening scenario in Europe.

Able Archer’25 mitigates and adapts to stressed conditions, but is likely futile in the extreme ones — as the 1980s exercises themselves were.

The name is also a historical wink: in 2025, Europeans once again find ourselves resigned spectators to decisions made in our name and not necessarily in our best interest.

Disclaimer

This page reflects my own personal research and is presented for informational purposes only.

It is not an investment proposal or a performance representation. It does not constitute financial advice or a solicitation. I do not manage third-party capital.

Institutional investors, hedge funds, proprietary trading firms, and family offices may contact me regarding potential IP licensing and related services if interested. All intellectual property related to these models and methodologies belongs to M. Emmanuel.

This web page is not intended for retail investors. These models are not available to retail investors. Related retail inquiries will not be considered.